Table Of Contents

- What is Debt?

- How Does Debt Work?

- Good Debt vs. Bad Debt - What is the Gist?

- A: Examples of Good Debt

- B: Examples of Bad Debt

- C: The Key Differences of Good Debts and Bad Debts

- Things You Need To Know About Debt ? DEBT 101

- A: Secured Debt

- B: Unsecured Debt

- C: Revolving Debt

- D: Mortgages

- E: Instalment Debt

- Frequently Asked Questions on Debt

- Final Thoughts On Debts

- Read Also:

- What is Debt?

- How Does Debt Work?

- Good Debt vs. Bad Debt - What is the Gist?

- A: Examples of Good Debt

- B: Examples of Bad Debt

- C: The Key Differences of Good Debts and Bad Debts

- Things You Need To Know About Debt ? DEBT 101

- A: Secured Debt

- B: Unsecured Debt

- C: Revolving Debt

- D: Mortgages

- E: Instalment Debt

- Frequently Asked Questions on Debt

- Final Thoughts On Debts

- Read Also:

What Is Debt? Definition, Types, Examples, and How It Works

Debt is money that people, businesses or governments borrow and promise to pay over time, usually with interest. It allows an individual to afford houses, education, business, and other unplanned expenses.

However, if you borrow too much or don’t manage your money well, it can cause financial problems and hurt your long-term stability. That?s why understanding debt is crucial for everyone so that you can make informed decisions.

In this guide, you will learn what debt is, the types of debts, and the difference between secured and unsecured options. So, let?s begin!

What is Debt?

Debt refers to an obligation that occurs where one borrows money and makes payments of the debt for a certain period. Individuals, corporations, and even governments utilize debt in meeting various needs.

Some of the most common types of debt include –

- Mortgage loans

- Credit card debt

- Student loans

- Personal loans

- Auto loans

- Business loans

Generally, debt falls into two categories:

| Secured debt | It is backed by a type of collateral, such as your house or land. |

| Unsecured debt | It does not require any kind of asset as security. |

But, we will talk more about them later in the article.

How Does Debt Work?

Debt works through a type of agreement between a lender and a borrower. The latter gets the funds upfront and agrees to repay the amount (known as principal) within due time. However, the lender might also apply a percentage of interest and fees to the agreement. In that case, the borrower will have to repay more money than they had initially taken.

The exact terms, however, vary depending on the type of debt you have applied for. But the process usually stays the same:

| Steps | What happens |

| 1. Borrowing the money | An individual or a business applies for money from a lender to make a purchase or investment. |

| 2. Term agreement | Both parties have to agree on key terms, including the loan amount, interest rate, repayment period and payment schedule. |

| 3. Repayments begin | The borrower starts repaying the debt through monthly/yearly instalments. It may include both the principal and the interest. |

| 4. Obligation completed | Once they have repaid the debt entirely, the borrower will not be contractually bound to pay the lender. |

| Note: If you miss payments, it might result in late fees, damage to your credit score, higher interest cost, and much more. If you had contracted a collateral to your debt, you may lose it as well. |

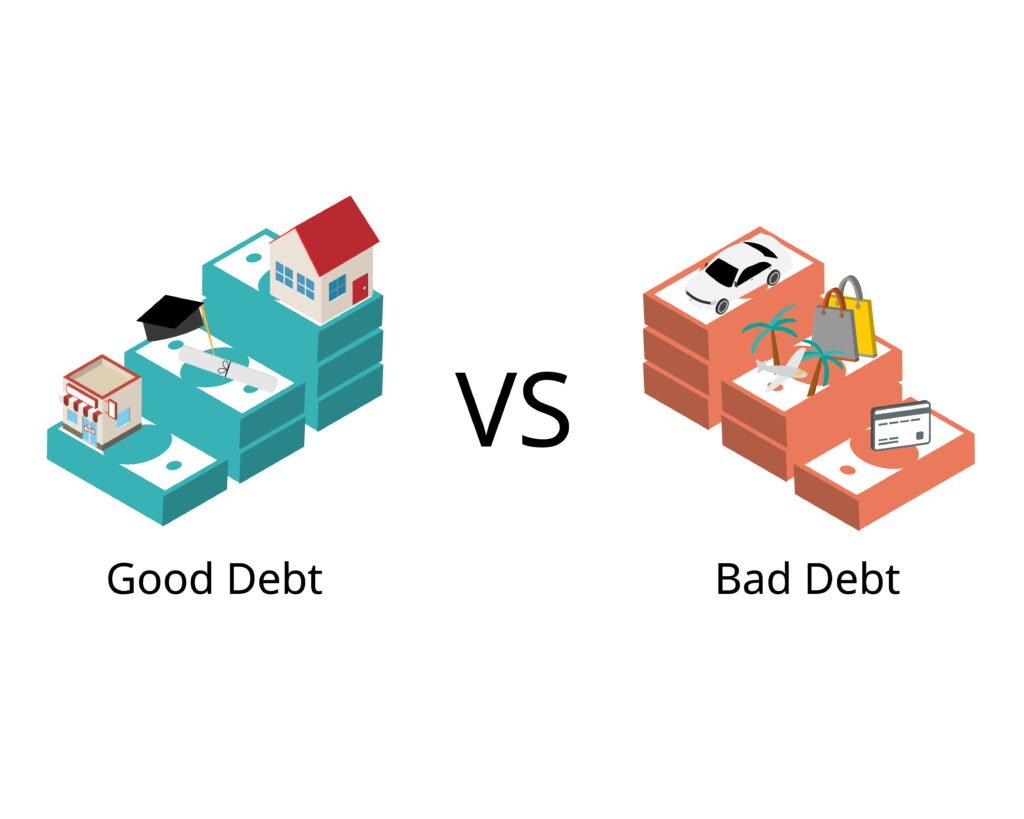

Good Debt vs. Bad Debt – What is the Gist?

Before we jump into the types of debts, let?s first distinguish what?s good and what?s bad. In essence, a good debt is something that helps you accomplish something valuable. On the contrary, a bad debt results in you losing the product?s (or whatever you used the money for) value over time.

A: Examples of Good Debt

If you?re trying to buy something that?s going to provide a great long-term value, we can consider it as good debt. Some examples of it are –

- Student loans to pay for your education

- Mortgage loans to buy a new home

- Business loans to grow or start a business

B: Examples of Bad Debt

Bad debts usually lose their value quickly or tend to come with a high interest rate. Here are some common examples –

- Payday loans

- High-interest credit card debt

- Debt used for unnecessary purchases (expensive vacations paid with credit cards or the latest gadgets that you can?t afford upfront)

- Borrowing more than you can repay while saving money

C: The Key Differences of Good Debts and Bad Debts

Some of the differences between these two debt personas are:

| Good debt | Bad debt |

| Can help you increase income or build assets | Often used for short term needs |

| Tends to have lower interest rates | Comes with higher interest rates |

| Can support long-term financial goals | Can lead to financial stress |

| Examples: Student loans and mortgages | Examples: High-interest credit cards and payday loans |

| Note: Remember, debt itself is not a good or a bad thing. The real difference is you, how you intend to use it, and whether you can repay it responsibly. |

Things You Need To Know About Debt ? DEBT 101

Debt comes in many forms. Some of them are backed by a collateral, while others can be requested depending on your credit score.

Here are some of the options you can choose from:

A: Secured Debt

Secured Debt is when the borrower agrees to give up a part of his asset or property in order to take the loan. While providing a secured debt, a credit check is a must. Some examples of a secured debt include –

- Mortgages

- Home equity loans

- Auto loans

| Note: If you fail to repay the debt, the finance company will sell the asset (collateral) to recover the money. |

B: Unsecured Debt

As the name suggests, it is very much the opposite of secured debt; there is no collateral for unsecured debts. And contrary to the popular belief, credit unions, banks, and various other financial institutions issue unsecured debt. Some examples of the same include:

- Credit cards

- Personal loans

- Student loans

| Note: As unsecured debts don?t include the collateral system, they usually come with a higher interest rate. Also, the approval of this type of loan will be based on factors like your income, credit history, and the ability to repay. |

C: Revolving Debt

Revolving credit allows a borrower to have access to money up to a pre-decided amount of credit. As the money is paid back, more credit is made available. Some of these include –

- Home equity lines of credit (HELOCs)

- Credit cards

| Note: As you pay down the balance, your available credit is restored, allowing you to borrow again up to your credit limit. |

D: Mortgages

In the case of mortgages, the collateral is the home – as they are only used for real estate purchases. Mortgages have the lowest interest rate when it comes to debts. You will also get around 15 to 30 years (depending on the lender) to pay off your debt. However, if you cannot do it, the lender will take your house away.

E: Instalment Debt

A term loan, also known as installment debt, is a kind of loan where payments are made at regular intervals until the entire loan balance has been paid back. Payments generally consist of the principal and interest components.

Some common examples of instalment debt includes:

- Mortgages

- Personal loans

- Student loans

- Auto loans

Frequently Asked Questions on Debt

These are some of the most asked questions by our readers. So, we?ve listed all of them at one place and will be answering the same one by one.

The maximum Loan Amount is nothing but the total sum of money a borrower can borrow. The maximum loan amount depends on several factors but mainly on the credibility of the borrower, the source of income of the borrower, and the collateral that he is willing to surrender.

Government-sponsored loans are loans that come with a few exceptions. While taking a Government-sponsored loan, the borrower does not have to match the criteria of good credibility, income source, etc.

A hard inquiry is just your full credit information and your credit score. It is mainly done by the lender before processing any loan application. A hard inquiry is also called a hard pull.

Final Thoughts On Debts

There you go, now you pretty much know everything about Debt. Managing Debt is one of the biggest financial challenges that youngsters are facing these days.

So it is very important for them to know all the little details about Debt so that they can learn to manage their debts better. I hope you have found this article informative and that it has added some value to your life.

Disclaimer: This article is for educational purposes only and should not be considered financial, tax, or legal advice. Please consult a qualified financial advisor before making borrowing decisions.

Read Also:

Why High-Performance Computing Is Becoming Essential

Crypto30x.com Explained: What It Promises, and What You Should Actually Pay Attention to

What Is a 529 Plan? Definition, Types, Benefits, and Rules

Footography: What It Is and How to Actually Make Money From It

Leave A Comment